–

Will you offer us a hand? Every gift, regardless of size, fuels our future.

Your critical contribution enables us to maintain our independence from shareholders or wealthy owners, allowing us to keep up reporting without bias. It means we can continue to make Jewish Business News available to everyone.

You can support us for as little as $1 via PayPal at office@jewishbusinessnews.com.

Thank you.

Last month, In January, Paul Singer’s Elliott Management, an activist hedge fund, had made several demands of yet another Silicon Valley company, this time manufacturer of networking equipment founded in 1996 Juniper Networks .

Singer, whose hedge fund owns 6.2% of the US$13.5 billion market cap company, made his case for change at the time in a well-documented, twenty eight page, presentation, also made available to shareholders and to the public.

At the same time he prepared a slate of his own directors, threatening to move ahead with a proxy contest if his demands were not met. Since Juniper’s profits and share price have stagnated in recent years, this was a relatively soft target for Elliott Management, and it should come therefore as no real surprise that we learned yesterday that management was throwing in the towel early.

Dressed up in corporate speak Juniper announced it had put in place a new “integrated operating plan” to:

• focus strategically on highest growth opportunities in networking as customers migrate to High-IQ Networks and best-in-class cloud environments which plays to Juniper’s strengths (corporate speak for getting rid of low margin business even at the expense of lowering revenues).

• optimize its One-Juniper structure and reinvigorate the company’s heritage of a mission-driven culture (corporate speak for slashing overheads)

• enhance operational efficiency intendended to result in a 25% operating margin by 2015 nearly 6 points better than 2013 (though they don’t quite say how).

• return more capital to sharholders, with a minimum of US$3 billion of capital in the next three years, including more than US$2.0 billion in the coming twelve months ( a key Elliott demand)

• commence a regular US$0.10 per share quarterly dividend in the third quarter of 2014, with the intention to grow it over time (another key Elliott demand)

• appoint two new highly qualified independent directors to be to Juniper’s board (to be Elliott’s nominees)

Juniper has agreed that the two new directors nominees will be Kevin DeNuccio and Gary Daichendt, both of whom are Elliott Management’s nominees and who have lots of experience in the networking industry. Cutting overheads and returning plenty of cash to shareholders were two other key demands of Paul Singer’s as well.

–

–

Juniper’s CEO, Shaygan Kheradpir, who only just joined Juniper at the beginning of January, had immediately signaled he was in favour of change once Elliottt came calling and yesterday he emphsasised the moves reflected input from a broad sampling of stakeholders in the company, including employees and major shareholders.

Yesterday Kheradpir reiterated that “I joined this phenomenal company as an agent of change to enable Juniper to realize its potential through a more focused, agile, connected, and execution-oriented structure optimized to capture the significant and growing opportunity we see before us.” (corporate speak perhaps for “if you can’t beat them join them”).

These steps have now satisfied Elliott Management, which has promised to vote for the new board at the upcoming Annual General Meeting. So after a lot of conversation a proxy battle has been averted, at least for the moment.

Jesse Cohn, portfolio manager at Elliott Management and Paul Singer’s principal partner in several of his activist moves, was even given a very prominent voice in the Juniper announcement, saying yesterday “Today’s announcement is an incredibly positive development for Juniper and its shareholders. Shaygan and his team have developed a thoughtful and highly value-accretive plan to invest for growth, significantly streamline and target the operations, and meaningfully return capital to shareholders.”

“Further, Shaygan and the Board, which will be adding two leading operations-focused executives, have impressed us with a focused commitment to accountability and execution of the plan. Elliott is highly optimistic about the Company’s future and looks forward to supporting Juniper in its continued focus on creating shareholder value.”

Nokia May Throw A Curve Ball

While there are smiles all round at the moment, it will all be driven by future results, and already there are signs of possible trouble for Juniper coming a little bit out of left field. Germany’s Manager Magazin Online has been reporting that Finnish company Nokia may want to buy Juniper and apparently has even made preliminary approaches to them late last year. Nokia is about to become flush with US$7 billion of extra cash once it closes its own deal to sell the Nokia mobile handset business to Microsoft, announced last year.

For Nokia that could certainly also be a very good way to quickly expand its’ networking business, Nokia Solutions & Networks (NSN), which is soon to be its largest division, and also to get rid of the cash coming from Microsoft before others try to get their hands on it.

With Juniper’s current market cap of around US$13.5 billion, for Nokia to already have more than half the cash it needs on hand could be a powerful enabler. To allow for some sort of premium, and in order not to borrow too much for the rest, Nokia might probably need to offer a cash and stock deal, plus have access to Juniper’s own US$3 billion in existing cash, post-merger. But precisely that kind of transaction may quite possibly already be on a number of people’s minds, including perhaps Elliott Management’s. For Paul Singer it would certainly be a very elegant form of exit. We shall certainly watch with interest how it all unfolds during 2014 therefore.

So far all parties concerned have of course refused to comment on any such idea.

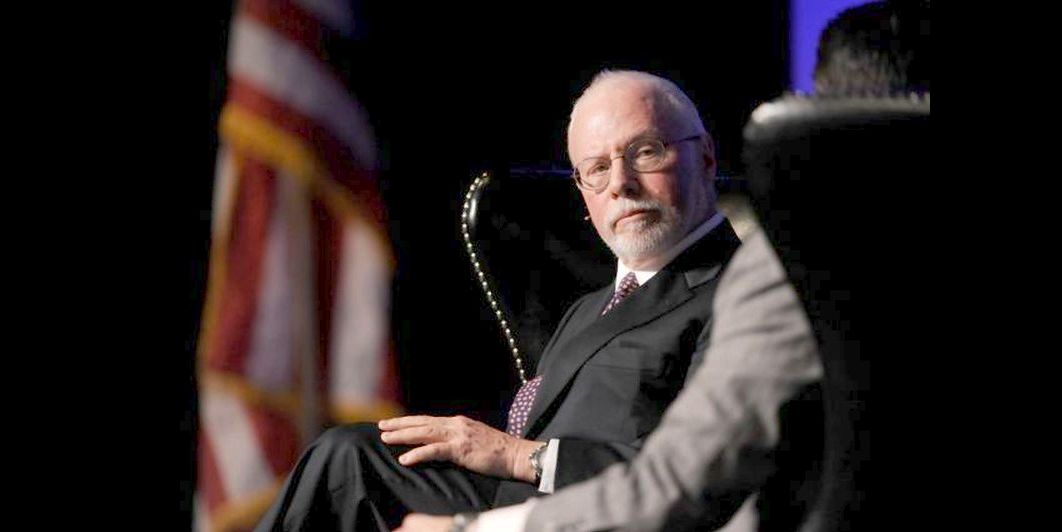

About Paul Singer

Paul Singer, 68, grew up in a Jewish family in Tenafly, New Jersey, one of three children of a Manhattan pharmacist and a homemaker. He earned a Bachelor of Science degree in Psychology from the University of Rochester and a Doctor of Jurisprudence from Harvard Law School.

After that, he spent the next four years working in corporate laws firms and the investment bank Donaldson, Lufkin & Jenrette before going ougt on his own to found Elliott Associates in 1977, making it one as the oldest hedge funds under continuous management with today US$20 billion under management. A key investment strategy of Elliott’s is buying up distressed debt cheaply and selling it at a profit, or tenaciously litigating for full payment – as we see in the case of his Argentine bonds.

According to the New York Times at a conference once in Las Vegas he has said his most important attribute as an investor was “existential humility”. “What am I missing ?” is a much more important question than “How cool am I ?” he told a rapt audience, which filled the grand ballroom of the Bellagio.

For hedge fund investors, however, it has been Mr. Singer’s performance as a money manager that is of greater interest. He has returned an average of 14 percent a year, over 35 years, and apparently has only lost money in two years: in 1998 and during the financial crisis of 2008, when he lost just 3 percent, according to the New York Times. “One of the biggest enemies of our long term portfolio performance is ourselves, ” he said.

–

{kind=link}