–

In an ideal world, nothing beats a savings account. You take your hard-earned money, hand it over to the bank down the block, and watch as your account balance steadily grows over. Unfortunately, in a world where even a 0.5% rate on a savings account is rare to non-existent, this is going to hurt you over time. If the interest you are receiving from the bank is less than the inflation rate (generally 2-3% per year over the past decade) you are losing money each and every day you keep your money in the bank. The balance might not change, but the real value is most certainly declining as your interest income fails to ‘make you whole’ against increases in the costs of goods and services across the economy.

Will you offer us a hand? Every gift, regardless of size, fuels our future.

Your critical contribution enables us to maintain our independence from shareholders or wealthy owners, allowing us to keep up reporting without bias. It means we can continue to make Jewish Business News available to everyone.

You can support us for as little as $1 via PayPal at office@jewishbusinessnews.com.

Thank you.

Dar Sandler Davide De Micco

So what do you do? Well, most people venture into the world of investing, the world of MSNBC, Jim Cramer, Wall Street Journal headlines, and Federal Reserve announcements. The number of choices, and potential risks, can be bewildering. You might be so put off by the dangers of investing that you find yourself walking back to that bank on the corner, happier dealing with a risk you know than an “unknown unknown”, as Donald Rumsfeld would have so aptly described it.

Or, you could seek the services of an Investment Advisor, and let somebody else tackle these issues for you. It’s the same way that you hire a plumber to fix your pipes, a mechanic to fix your transmission, and a baker to bake your bread, even though you might be able to do these things yourself with enough time and energy (and loads of patience).

Most investment advisors are going to try to optimize the “Sharpe Ratio” of your portfolio. That ratio describes the risk-adjusted returns of your assets. If you’re interested in the nitty gritty, it’s the excess return of your portfolio, minus the risk-free rate (government bonds), divided by the standard deviation of your returns. To put that in plain English, how well are you being compensated for the risk that you’re taking by buying investment securities, rather than leaving your cash in a bank account? The higher the Sharpe Ratio, the better you are being compensated for that risk.

To achieve a nice healthy Sharpe Ratio, most investment advisors are going to advise you to follow the classic 60/40 model – 60% equities, 40% bonds or fixed-income securities. The idea here is to hold two different asset classes whose returns do not correlate (i.e., do not follow each other), and then adjust the mix of those two classes over time to make sure you’re taking on the right amount of risk. Equities are more volatile; think of how the stock market swings around every day based on the latest set of earnings releases (or iPhone announcement). Fixed-income securities, on the other hands, tend to perform more smoothly over time.

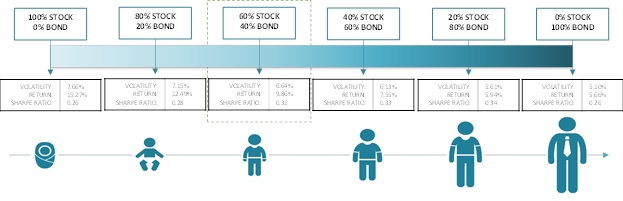

Younger investors with more time before retirement will take on more risk, and have a higher percentage of equities in their portfolio. As investors near retirement, the portfolio balance is shifted toward fixed-income instruments, to provide smoother and less volatile returns. After all, you don’t want to be a few years from retirement and see a large percentage of your assets disappear in a stock market bubble!

Here’s a graphic to give you a better idea. For now, just pay attention to the changing allocations, and how the Sharpe Ratio changes over time.

–

So what’s wrong here? After all, you’re diversified, you are adjusting your mix of assets to take on the ‘right’ amount of risk, and you’re being ‘smart’ about not being in a risky position too close to retirement. This is an industry standard model, followed by tens of millions of investors around the US!

Unfortunately, something is rotten in the state of Denmark. Here are a few things you might want to think about:

- If you look closely in the graphic, you’ll see the Sharpe ratio changes as you move through the different time periods. In other words, you are getting a better bang for your buck with a mix of stocks/bonds in the middle, than having just one or the other at the two extremes. This is a problem because during the early and later periods of this portfolio you are not getting ‘paid’ as well for the risk you are taking.

- Different kinds of assets involve different kinds of ‘bets’ on what’s going to happen in the economy. Stocks are a bet on a booming economy, while bonds are a bet on low inflation. Your portfolio mix changes over the life-time of the portfolio. At each end of the spectrum in the 60/40 portfolio (100% stocks vs. 100% bonds), you are locking yourself into betting on a specific outcome in the economy. It would be like writing on a sheet of paper how much money you will put in the pot in a poker game, before you’ve even seen your hand!

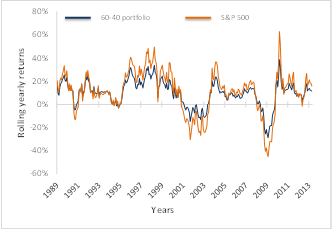

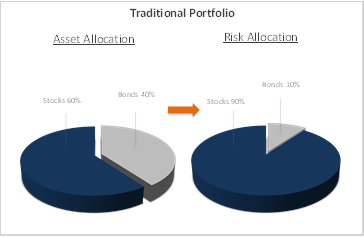

- You might think that you are protected nonetheless by following this portfolio, since you are splitting your money across different asset classes. But the numbers don’t support that. Stocks are significantly riskier than bonds. The result is that even when you are 60% stocks and 40% bonds, “well-diversified”, almost all of the volatility/risk in this portfolio is coming from the stocks. You aren’t really diversified at all against the risks of holding a heavily stock-weighted portfolio. If you don’t believe me, take a look at the graphic below. If the 60/40 portfolio is diversified, then why does its performance practically follow in lockstep with the S&P500? And take a look at the next chart – a portfolio that is 60% stock has 90% of its risk coming from the equity category.

Clearly something is wrong here. Your goal might be to take on the right amount of risk at the right time, and to be hedged against the latest mishaps in the economy. But the 60/40 portfolio that’s being promoted by most of the investment industry is setting you up for a fall. At the very least, there are some pretty serious limitations in this approach that you might not have been aware of until now. We’ll be continuing to talk about this in later blog posts, along with a new way of thinking about investing that addresses the shortcomings that we discussed above.

Edited by: Simon Cartoon